For people nearing retirement, a large redundancy payout can feel like both a lifeline and a heavy responsibility. When that money goes straight into a pension, the decision about how to invest it suddenly feels much bigger. One wrong move can feel like it could undo years of planning, especially for those hoping they are finished with full-time work for good.

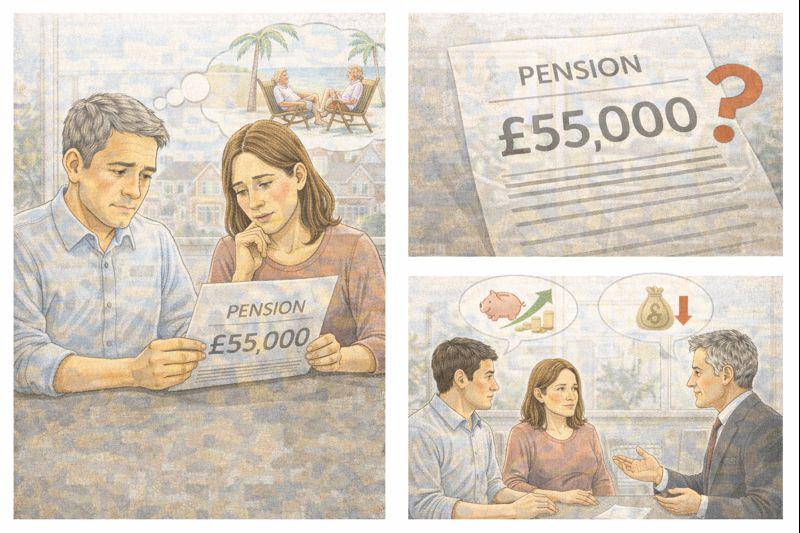

That is exactly the situation one person recently found themselves in. After taking £30,000 tax free from a redundancy package, they were left with a £55,000 lump sum. Instead of keeping it in cash, they chose to pay it into their existing pension. They already had a similar amount in that pension from regular monthly contributions, meaning this one decision would effectively double the size of their pot.

They explained that they could technically access the pension in around a year, once they turn 55, but they do not plan to touch it yet. The hope is to stop working altogether and live off savings and investments, a goal often described as early retirement or financial independence.

At the moment, all of their investments are in high-risk global equity funds. These are growth-focused investments that can rise sharply over time, but they can also fall hard during market downturns. On top of the pension, they also have around three to four years of living costs held in cash, as well as a small defined benefit pension that will start paying out from age 60.

The big question they asked was simple but important. Should this new £55,000 be invested in lower-risk funds to reduce the chance of big losses, or should it stay fully invested in high-risk equities like the rest of the pension? Were they being sensible, or just overthinking things?

This is a question many people face as they approach retirement, and it comes down to balancing growth, risk, and peace of mind.

One key point that often gets missed is that money does not change just because it arrives as a lump sum. Once it is inside the pension, it becomes part of the overall pot. What really matters is not where the money came from, but how much risk the total portfolio is taking and whether that risk matches the person’s situation.

In this case, the person is not starting from zero. Having several years of cash already set aside is a strong position. That cash acts as a buffer. If markets fall in the first years of retirement, they do not need to sell investments at a bad time to pay bills. This alone reduces a lot of the danger that worries people about staying invested.

The future defined benefit pension also changes the picture. Knowing that a guaranteed income will arrive at age 60 provides stability later on. That income can take pressure off the investment pot, making it less risky overall than it might appear on the surface.

However, there is also the emotional side. Investing £55,000 all at once can feel very different from drip-feeding money in each month. If markets were to fall sharply soon after investing, seeing a large drop linked to one decision could be very stressful, even if it is a normal part of investing. That stress can sometimes lead to panic decisions, which can cause more damage than the market fall itself.

This is why some people choose to reduce risk for part of their money as they get closer to retirement. It is not always about chasing the highest returns. Sometimes it is about making sure you can stick with your plan when things go wrong.

One practical way to think about it is to focus on when the money will be needed. If the £55,000 is money that will not be touched for ten years or more, staying invested in equities can make sense. Over longer periods, shares have historically offered better growth than bonds or cash. If the person is confident they will not need this money early on, keeping it in growth funds may fit their goals.

If, however, this money might be used in the first few years of retirement, taking less risk becomes more attractive. Early retirement is when market falls can do the most harm, because withdrawals are happening at the same time as losses. Holding some lower-risk investments can help smooth that risk.

Many people settle on a middle option. Instead of choosing all high risk or all low risk, they split the lump sum. Part stays in growth funds, and part goes into lower-risk or balanced investments. This does not eliminate risk, but it spreads it out and can make the overall journey feel more manageable.

Another approach is to think about the pension as a whole and rebalance slowly over time. Rather than changing everything at once, some people keep the money invested as it is now and gradually reduce risk once they actually stop working or start drawing income. This avoids trying to time the market and spreads decisions out over several years.

It is also worth remembering that risk labels on funds are only guides. A fund described as lower risk can still fall in value, and a global equity fund may be more diversified than people expect. Looking at what the fund actually invests in matters more than the number attached to it.

The fact that this person hopes not to work again makes protecting what they already have especially important. At this stage of life, avoiding large losses can matter more than squeezing out extra growth. But because they have cash reserves and a future guaranteed pension, they are not relying entirely on this pot in the short term.

So are they overthinking it? Probably not. Asking these questions is a normal and healthy part of planning for retirement. Overthinking would be constantly switching investments or reacting to every market move. Taking time to make one careful decision is simply being cautious.

A sensible next step is to step back and look at the full picture. How much money is in cash, how much is invested, and how much guaranteed income is coming later? From there, the lump sum can be invested in a way that keeps the overall balance where it feels comfortable.

For some, staying fully invested brings confidence in long-term growth. For others, moving part of the money into lower-risk funds brings peace of mind. Both choices can be valid. Early retirement is not just about numbers on a screen. It is about feeling secure enough to stay retired, even when markets are rough.

In the end, the best decision is the one that allows someone to sleep at night and stick with their plan for the long run.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Leave a comment