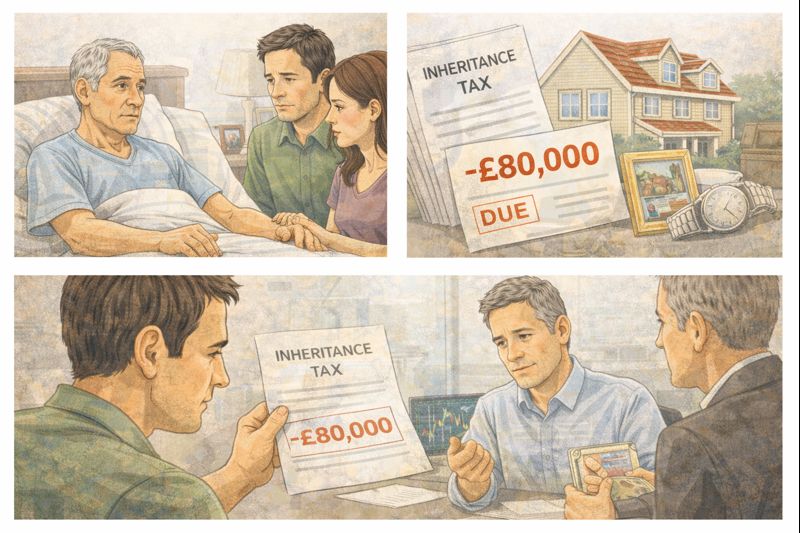

When a parent becomes terminally ill, families are often pushed into planning conversations they never expected to have so soon. Alongside the emotional weight of what is coming, there is suddenly pressure to understand complicated financial rules, legal processes, and large sums of money. For many people, inheritance tax becomes the most frightening part of that picture, especially when most of the estate is tied up in property or long-standing family assets rather than cash.

That is the situation facing a 26-year-old woman who decided to start planning early, knowing that once grief sets in, dealing with paperwork and financial decisions would be far harder. Her parent’s estate is estimated at around £2 million, but very little of that value exists as money in the bank. Instead, it is spread across several houses, a family business, and farmland that has been in the family for generations.

The first concern she raised is one that confuses many families. Inheritance tax is usually due within six months of death, but if the money to pay it comes from selling property, how does that work? How can you sell a house if you technically cannot access or transfer it until the tax is paid? And if you are named as an executor, what are you actually allowed to do?

The reality is less impossible than it first appears. Executors are legally allowed to sell property that belongs to the estate. In fact, this is very common. The property does not belong to the beneficiaries yet, it belongs to the estate, and the executor’s job is to use estate assets to settle debts and taxes before anything is passed on. You do not need to personally own the house to sell it. The estate sells it, and the money raised is then used to pay inheritance tax and other liabilities.

Another important point is that inheritance tax does not always have to be paid in one single lump sum immediately. While HMRC expects payment within six months, there are options to pay the tax in instalments for certain assets, particularly property. Interest is charged, but this option can ease pressure and prevent rushed or forced sales while everything is being worked out.

In this case, the estate is particularly complex. It includes a small family business worth around £350,000 that has been passed down through generations. One sibling plans to keep the business running and intends to take out a loan to buy it from the estate. There is also farmland worth about £300,000, along with machinery that is essential to continue farming. Selling this land would damage the business and the family legacy.

There are also three houses built by the parent, valued at roughly £550,000, £400,000, and £400,000. Two of these are already lived in by family members. One of the £400,000 homes was gifted to the siblings less than two years ago, which means it still counts as part of the estate for inheritance tax purposes. Many people are surprised by this rule. In the UK, gifts made within seven years of death can still be taxed, depending on timing and circumstances.

The plan is to sell the £550,000 house to help cover the tax bill, but even that will not be enough on its own. This is where families often feel stuck and overwhelmed.

What many do not realise is that estates like this may qualify for significant tax reliefs. Business Property Relief can reduce or remove inheritance tax on qualifying business assets. Agricultural Property Relief can do the same for farmland. These reliefs exist specifically to stop family businesses and farms from being broken up just to pay tax. Whether they apply depends on how the assets are used and structured, which is why professional advice is so important.

There are also specialist loans designed specifically for inheritance tax. These are often called probate loans or inheritance tax loans. They are usually short-term loans taken out by executors to pay the tax upfront. Once property is sold or other funds are released from the estate, the loan is repaid. These loans are commonly used in larger estates and are offered by specialist lenders rather than everyday high street banks.

Emotionally, this process is extremely hard. Planning how to pay inheritance tax while a parent is still alive can feel cold or wrong, even though it is practical. Many people feel guilt just thinking about it. But planning now can prevent far more stress later, when grief is fresh and decisions have to be made quickly under pressure.

It is also important to understand that inheritance tax is not designed to trap families in an impossible position. The system recognises that estates are often illiquid. That is why executors can sell assets, why instalment options exist, why loans are available, and why reliefs are built into the rules.

The most important step for families in this position is to get proper professional advice early. A solicitor or tax adviser who deals with estates of this size can calculate what tax is actually due, identify which assets qualify for relief, and help plan the order in which things should happen. In many cases, the final tax bill ends up being lower than families first fear once allowances and reliefs are applied.

For anyone reading this who is facing a similar situation, the key message is this: you are not expected to personally find hundreds of thousands of pounds overnight. You are allowed to use the estate to pay the estate’s tax. With planning, advice, and time, even complicated estates with little cash can usually be managed without destroying everything the family has built.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Leave a comment